Our journey to investing ran straight through a pandemic, a house purchase, and one important conversation…

At Element Ventures [now 13books], we focus on B2B fintech so it’s rare that we’ve had personal experience of using a product prior to investing. We must find other ways to validate the market need and customer experience. I often envy my consumer-focused peers who have the luxury of personal product use when investing. But this time was different – our journey to investing in Thirdfort ran straight through a pandemic, a house purchase, and a conversation with my wife.

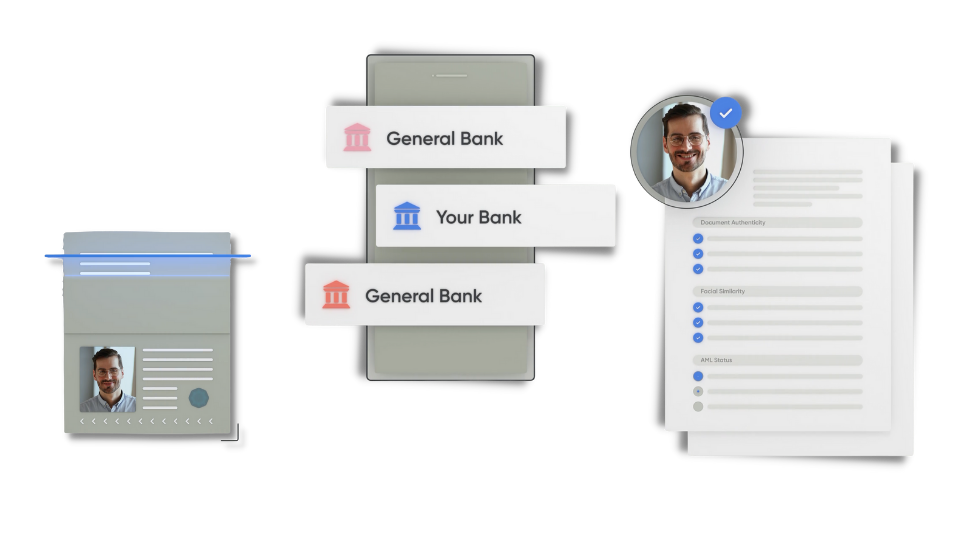

Deep into the pandemic we were buying a house and frantically trying to coordinate all the various parties involved during yet another lockdown. Among many other things this included onboarding to the estate agent representing our house seller (Knight Frank in this case), however this time the process was different. Instead of having to “mask-up” and go visit their offices to show our passports, they sent us a link to a new app – Thirdfort – which we used to digitally KYC and onboard remotely.

Once completed I remarked to my wife how easy it was and her reaction was “Yeah…we used Thirdfort to onboard our business to another law firm…it’s super easy”. And that was a cliché lightbulb moment, Thirdfort was solving a massive problem and the product was fantastic.

As it happens, I’d been introduced to Olly a year earlier by an existing angel, so we knew exactly who to harass about investing in the business. And so, we’re exceptionally pleased that Jack and Olly finally relented, and we can announce our participation in their Series A, led by the fantastic team at Breega and alongside leading founders from companies including ComplyAdvantage, Tessian, Fenergo, R3, Funding Circle and Fidel API.

The Problem

Banks and other large financial institutions are well served in innovation and modernisation in the KYC/AML space. Still, the obligations and regulations to ensure clients are known and money is clean stretch well beyond the borders of banks. One market that has been deeply underserved in this respect is professional services firms, especially those involved in high-value transactions such as property purchases. Lawyers, estate agents, accountants and others are all responsible for knowing their clients and where their money is coming from. Still, they often don’t have the technology budgets and organisations to build proprietary software or manage expensive enterprise-grade solutions.

Thirdfort was solving a massive problem and the product was fantastic.

As a result, the processes have remained painfully manual: take your passport to an office, send a PDF scan, or jump on zoom to hold up your passport all are woefully common ways of onboarding. Not only are these processes expensive and cumbersome for clients, but they are also prone to error – leaving professional services firms at risk of breaches and fines.

The professional services market was desperately in need of a modern KYC/AML solution that worked for both businesses and consumers. Money laundering was costing the UK economy alone £100bn annually! But money laundering is esoteric. We don’t see it, it doesn’t affect our day-to-day lives, and maybe KYC/AML is just a box ticking exercise that we don’t really have to worry about?

Except that wasn’t the experience for Jack and Olly – for them, watching a friend get defrauded out of £25,000, having been through all the “box ticking”, showed them this was a problem that had a real impact on people’s lives…and they set out to change it.

The Solution

They built Thirdfort, a risk management platform for professional services firms. Using a proprietary risk engine and open banking data, the platform offers digital onboarding and AML checks for the legal and property sectors and will soon be extended to mortgage broking, accounting and wealth management. The team also plan to expand the product into secure payments to create a seamless end-to-end modern transaction experience for high-value purchases.

Businesses using Thirdfort get a customisable product which aggregates multiple KYC data sources (address match, PEPs, credit check, facial recognition, etc.) and uses open banking and payments data to execute enhanced AML checks allowing for rapid but highly accurate client onboarding at lower cost and user experience friction. For consumers, the experience moves from analogue to digital – you simply download the mobile app, connect your bank feed and input verification data, and that’s it, onboarding complete—no visiting offices to take copies of passports, no awkward emailing of bank statements.

Today Thirdfort serves over 700 businesses, including leading law firms DAC Beachcroft, Penningtons Manches Cooper and Mishcon de Reya, and property businesses Knight Frank, Strutt & Parker and Winkworth. The consumer app has been downloaded by over 500,000 people in the UK over the past two and half years!

The business has grown tenfold in terms of revenue and people since January 2020 and plans to expand its team from 94 to 150 by the end of 2022.

£15m to keep solving problems

The Thirdfort team have only just scratched the surface of the problems felt by their clients. Two immediate acute issues stand out: first, professional services firms onboard businesses as well as individuals and second, checking the Source of Funds for transactions is incredibly cumbersome and complex. So along with expanding their customer verticals, the Thirdfort team are also setting out to solve these challenges, and they have £15m in the bank to do it.

Jack and Olly are founders who care deeply about the Thirdfort mission, and in the short time we’ve spent with the team, we can see their passion permeate the whole business. Their speed and clarity of execution have been truly impressive, and we’re thankful to be along for the ride.